August 10, 2022

Experts:

Introduction

Amid rising prices, regulatory expansions, and large government spending increases, many policymakers and activists are searching for ways to increase Colorado’s affordability. Emboldened by the success of Proposition 116 in 2020, which reduced the state income tax rate from 4.63% to 4.55%, that measure’s sponsors have proposed another income tax cut of almost double its magnitude for the 2022 ballot.

Proposition #121, which would further reduce the state income tax rate from 4.55% to 4.4%, has qualified for the 2022 general election ballot and will receive its official proposition number by September 9

th

.

The reduction in the state tax rate would be retroactive for income earned in 2022 and is projected to reduce total state income tax collections over 2022 and 2023 by $572 million.

In this report, CSI outlines the details of Proposition #121 and projects the impacts it could have across the Colorado economy upon both the private sector and the state.

Key Findings

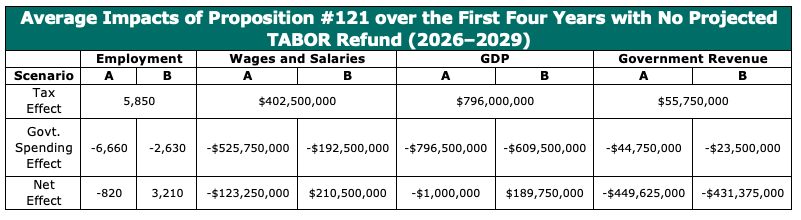

- Proposition #121 would save Coloradans $1.6 billion over the first 5 years after its passage. In 2023, taxpayers would save $767 million, which is more than in any other year—this is because both the 2022 and 2023 tax savings would be realized in 2023 without causing any corresponding reduction in the FY22 TABOR refund, which is already budgeted. In 2024, taxpayers will experience a net tax increase due to the interaction between the 2023 savings and the FY2023 TABOR refund, which would be distributed in 2024.

- Proposition #121 is not projected to reduce state government spending in either of its first two fiscal years because it offsets future TABOR refunds. Over those years, general fund spending is projected to increase by 13.4% from $16 billion to $18.2 billion. In future years with no TABOR refund, the tax cut will lower total revenue available for spending compared to the current baseline but will likely not cause nominal spending reductions between any two years.

- The largest one-year economic impact of Proposition #121 would occur in 2023, which is the year of the biggest net tax reduction. The dynamic impact of the tax savings in 2023 would be an estimated additional 9,110 jobs.

- Proposition #121 would increase private-sector employment and decrease government employment in the long run. The net impact on employment in 2026, the first year without a projected TABOR refund that the tax cut would offset, depends upon the degree to which the state government manages a smaller budget by reducing the growth in government jobs.

- The state would gain 2,520 jobs under Scenario B, whereby the state government does not cut any jobs and instead constricts spending elsewhere.

- The state would lose 1,590 jobs under Scenario A, whereby the state government cuts its employment to account for the reduction in its revenue.

Background

Current Income Tax Structure in Colorado

Most states have progressive income tax codes and seven do not tax income at all; Colorado is one of nine states which apply a flat income tax rate to residents at all income levels. The state applied a graduated income tax before 1987, at which point the various tax brackets were consolidated into a single rate of 5% due to a bipartisan legislative effort. That rate has since been adjusted down three times: twice due to TABOR provisions and once by Proposition 116, a citizen initiative passed in 2020. The effect of Proposition #121, if passed, would be to reduce Colorado’s current flat rate of 4.55% to 4.4%; the current rate has been effective only since the passage of Proposition 116, before which it had held steady at 4.63% since 2000.

The income tax regulation in Colorado is inclusive of individual, corporate, fiduciary, and partnership income; this will remain true regardless of Proposition #121’s fate.